Spain's Invisible Portfolio

Public pensions, housing, and the hidden architecture of Spanish wealth.

Core thesis

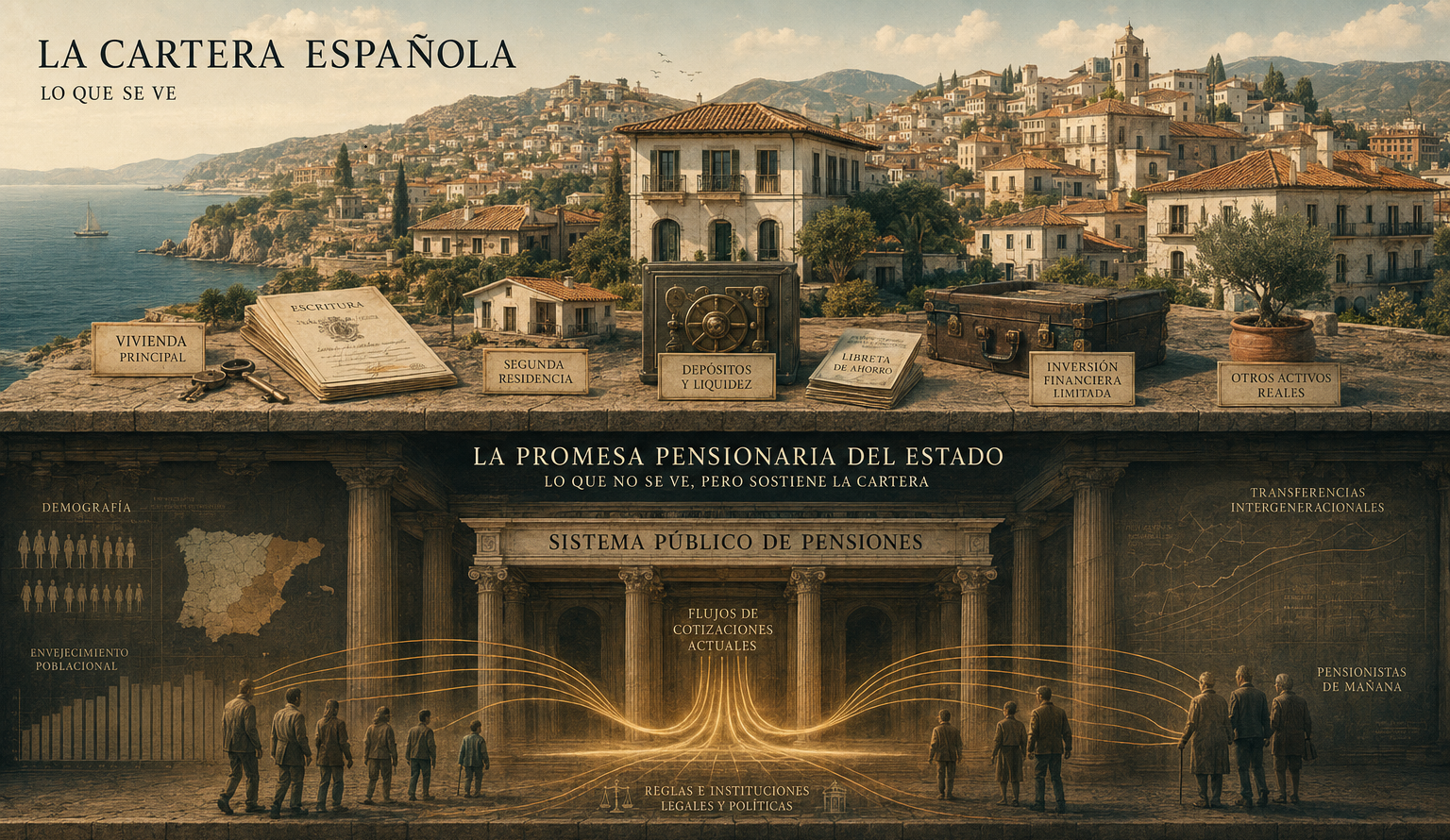

Spain’s patrimonial architecture

For decades, Spanish household wealth was built around private housing plus a very large public promise of future income.

Political and institutional capital

The public pension functions like a major implicit defensive asset, but it rests on demography, employment, public debt and institutional stability.

From political wealth to financial capital

If the state’s protective capacity weakens in relative terms, private financial capital will have to carry more of that burden.

Every society builds wealth around what it trusts. Some did it through land and agrarian rents. Others through trade, financial markets or productive capital. A country’s patrimonial structure is never accidental: it reflects its history, its institutions and its relationship with risk.

Spain is often described as a patrimonially conservative economy. Households concentrate a large share of their wealth in housing, keep a high weight in deposits, and show relatively limited exposure to equities, index funds and capital markets.

From an Anglo-Saxon perspective, this structure can look incomplete: too much brick, too little equity, too little financial sophistication. But that reading misses a decisive piece of the Spanish patrimonial balance sheet.

A critical share of household wealth does not appear in private portfolios. It is not in a brokerage account, an investment fund or an individual retirement account. It is embedded in a public promise of future income.

For decades, Spanish households did not need to build a large private financial portfolio because part of that portfolio had already been socialized through the state. At an aggregate level, the Spanish household portfolio was never simply real estate heavy. It was a blend of private housing and future public income.

The problem is that this patrimonial architecture depended on a set of balances that are now starting to tighten: demographic aging, lower potential growth, rising fiscal pressure, elevated public debt, and an increasingly delicate relationship between workers, pensioners and the state.

For decades, the state acted as the great defensive pillar of the Spanish patrimonial balance sheet. The defining question of the coming decades is what happens if that function loses relative strength.

“Spain’s visible wealth sits in housing. Its invisible wealth sits in the pension promise.”“Spain does not just have households that own homes. It has households with an enormous implicit position in the state.”

Wealth that does not appear on the balance sheet

The OECD calculates a metric called net pension wealth: the present value of expected future public pension payments, net of the taxes and contributions retirees are expected to pay on them.

This figure is not liquid money. It is not an asset that can be sold, inherited or transferred. But it does represent something economically real: a promise of future income.

In Spain, that promise is exceptionally large. Net pension wealth amounts to more than twenty times annual gross earnings, one of the highest readings among developed economies.

That changes the reading of the Spanish portfolio entirely. If we look only at private assets, we see housing, deposits and relatively limited market exposure. From an Anglo-Saxon lens, the picture can look conservative, incomplete and even financially underdeveloped.

But the picture changes radically once we include the part of wealth that never appears on the bank statement. Then a far more complex structure emerges: visible real assets, conservative liquidity, and a vast stream of future income politically guaranteed by the state.

Net pension wealth

Spain’s invisible household wealth is exceptionally large

Present value of expected future public pensions as a multiple of annual gross earnings. Spain stands out among developed economies because of the scale of this implicit future income — a crucial piece for understanding why the Spanish portfolio looks so different when we only observe private assets.

The distance between Spain and the OECD average is not a technical detail. It is a structural difference in how a society organizes future security.

Source: OECD · Net pension wealth · 2022

The public pension as invisible fixed income

From a patrimonial perspective, the public pension resembles a very large implicit position in long-duration sovereign fixed income more than it resembles a simple subsidy.

It has the core traits of a state bond: it promises recurring future cash flows, depends on the fiscal capacity of the issuer, rests on institutional rules, and reduces the need to generate private income during retirement.

But it differs in one crucial respect. It does not trade in a market. It has no daily price. It does not appear in an investment account. It cannot be sold, transferred or inherited. Precisely because of that, it tends to disappear from conventional patrimonial analysis.

Yet this invisible wealth profoundly shapes the way a society perceives risk, saving and future security. A household expecting a large public pension does not need to build the same financial architecture as an American household that must individually capitalize a much larger share of retirement.

The implication is deep. Two households with similar private balance sheets can have radically different patrimonial exposures once the economic value of future pension rights is taken into account.

The public pension does not eliminate the need for private saving. But it radically changes how a society thinks about risk, retirement and the accumulation of financial capital.

Spain is not just housing: it is housing plus state

Spain’s patrimonial architecture can be summarized as a blend of visible assets and implicit institutional wealth. On the surface, we see the primary residence, second homes, deposits, and a relatively limited financial layer. Beneath that surface lies another asset: a very large public promise of future income.

That combination explains much of Spanish financial culture. Housing works as a patrimonial anchor because it is tangible, stable, inheritable and socially legitimate. The public pension works as an intergenerational stabilizer because it lowers the perceived urgency of future insecurity.

For decades, both pieces reinforced one another. Housing provided visible patrimony. The state provided expected future income. Together they generated enough stability that many households never felt compelled to develop large private financial portfolios.

That is why direct comparison with the United States can be misleading. In the U.S., a much larger share of future security depends on market assets: private retirement plans, mutual funds, equities, ETFs and individual capitalization. Retirement outcomes are much more directly tied to market behavior.

In Spain, by contrast, a significant part of that defensive function was historically externalized to the state.

The difference is not only financial. It is cultural, political and institutional. They are two different ways of organizing patrimony.

The state as part of the national portfolio

The core idea is simple, but its implications are enormous: the state forms part of the patrimonial portfolio of households.

Not as a tradable asset, but as an institution that transforms present contributions into future rights. The public pension operates as an invisible layer of the national balance sheet.

This helps explain why Spain historically developed a different relationship with financial risk. If the defensive base of retirement is already partly guaranteed by the public system, the private portfolio can lean more heavily toward familiar and real assets: housing, property, bank liquidity and conservative saving.

Seen through this lens, the Spanish portfolio is not merely an unsophisticated portfolio. It is a different patrimonial architecture.

The standard error is to compare only visible financial assets while ignoring the economic weight of the implicit pension promise. Once that piece enters the analysis, the Spanish structure stops looking anomalous and starts looking like a coherent wealth system.

Visible wealth lived in brick. Invisible wealth lived in the social contract.

A 60/40 portfolio that was never called a portfolio

In portfolio-theory terms, this leads to a provocative interpretation. The traditional Spanish family never built a modern financial portfolio in the Anglo-Saxon sense. It built something else: a hybrid structure of housing, conservative liquidity and future public income.

Housing served as the main patrimonial asset. Deposits functioned as a reserve of stability and liquidity. And the public pension supplied an expected stream of relatively stable retirement income.

It is not a conventional 60/40 portfolio. But functionally it is closer than people usually admit. There is a dominant real-asset block and a major implicit stabilizer of future income.

The difference is that the defensive asset did not sit inside an investment account. It sat inside the institutions of the state.

For decades, millions of Spanish households participated in a form of patrimonial diversification that was never explicitly understood as portfolio theory, yet in practice fulfilled a similar purpose.

The great paradox is that a society that appeared lightly financialized had, without naming it as such, built one of the most distinctive patrimonial architectures in the developed world.

The fragility of the system

Not all pension systems work the same way. Behind each model lies a different way of organizing wealth, risk and economic security.

Broadly speaking, there are two major architectures: funded systems and pay-as-you-go systems.

In a funded system, financial assets are accumulated. Contributions are invested in equities, bonds, funds or other instruments that build an explicit retirement portfolio. Future pension outcomes depend largely on accumulated capital and the returns earned on those assets.

In a pay-as-you-go system, current workers’ contributions directly finance current retirees. There is no large individualized stock of financial assets backing each future pension payment. What sustains the system is something else: the continuity of the intergenerational contract.

Spain belongs essentially to this second model. The Spanish public pension system was historically built as an overwhelmingly pay-as-you-go structure, with a relatively limited role for private capitalization compared with other developed economies.

That helps explain why Spanish implicit pension wealth is so extraordinarily large. For decades, the state absorbed a very large share of the defensive function that, in other countries, sits much more heavily on private balance sheets and financial markets.

In other words, a fundamental part of Spanish household security was not backed by individually accumulated financial assets, but by the future capacity of the economy to keep supporting the system.

That is where the true fragility of this architecture appears.

In a funded system, the main risk is financial: poor returns, inflation, market volatility or outright market crises. But the assets exist, they have a price and they represent explicit property rights over accumulated capital.

In a pay-as-you-go system, the risk is far more diffuse and deeply political. Future stability depends on demography, productivity, formal employment, wages, tax capacity, public debt and the balance between generations.

As long as the active population was growing, wages were rising, and the worker-to-retiree ratio remained favorable, the system could expand without generating too much visible strain. But demographic aging slowly changes that equation.

The consequence is uncomfortable but essential: a huge part of Spanish households’ implicit patrimony depends on demographic and political balances that looked solid for decades, but whose foundations are gradually weakening.

That is why Spanish pension wealth is both powerful and vulnerable. It is not exposed to the daily volatility of financial markets, but to a much slower and harder-to-see volatility: the gradual erosion of the social contract itself.

A stock can collapse in days. A pay-as-you-go system can weaken over decades without ever producing a single visible moment of rupture.

Financial markets adjust immediately and transparently. Political systems usually adjust slowly: through inflation, higher taxes, later retirement ages, lower relative generosity, or gradual reforms that are difficult to perceive in the short run.

The deepest paradox is that the most important wealth block in the Spanish patrimonial balance sheet is also the hardest to value, monitor and protect. It does not appear in an investment account. It appears only in the collective confidence that future generations will keep the system standing.

Spain’s great patrimonial transition

The Spanish patrimonial equilibrium worked for decades because several forces moved in the same direction: economic growth, demographic expansion, housing appreciation and a broadly credible public promise.

But that architecture is starting to tighten. Population aging, rising fiscal pressure on labor, weaker housing affordability and uncertainty around future pensions are slowly changing the model.

That may push younger generations toward a different patrimonial structure. Not necessarily for ideological reasons, but out of economic necessity.

If the expected public pension loses relative strength as an implicit defensive asset, households will have to rebuild part of that security through private financial capital. That means more investment funds, more global equities, more private plans, more financial culture and a different relationship with market risk.

In other words, part of the stabilizing role historically performed by the state may gradually shift back toward private balance sheets.

Spain may be entering a historical transition from a model based on housing + state toward one with greater weight in private financial capital + global investment.

The transformation would not be merely financial. It would be cultural. It would change how households relate to saving, risk, retirement and the very meaning of economic security.

The defining question of the coming decades is not only how much Spanish financial wealth will grow. It is what happens when a society accustomed to relying on political wealth must start rebuilding a larger part of its security through capital markets.

The PFAtlas thesis

A portfolio is not just a list of assets. It is a theory of security. For decades, the Spanish theory was clear: own housing, keep liquidity and trust a relatively generous public pension.

That structure was not accidental. It reflected institutions, fiscal incentives, family culture, the labor market, the banking system and the welfare state.

The question now is not only whether Spaniards will invest more in equities. The deeper question is this: what happens when a society that built its security on housing and public pensions starts to doubt both?

That is where the new Spanish portfolio begins. And that transition — from brick to state, and from state to market — may become one of the defining patrimonial stories of the coming decades.

The PFAtlas thesis

A portfolio is not just a list of assets. It is a theory of security.

For decades, the traditional Spanish portfolio rested on housing, liquidity and a public promise of future income. If that promise loses relative credibility, the patrimonial architecture of the country will change with it.

That is where a new story begins: the transition from security rooted in brick + state toward one with more private financial capital, more global exposure and a different relationship with risk.